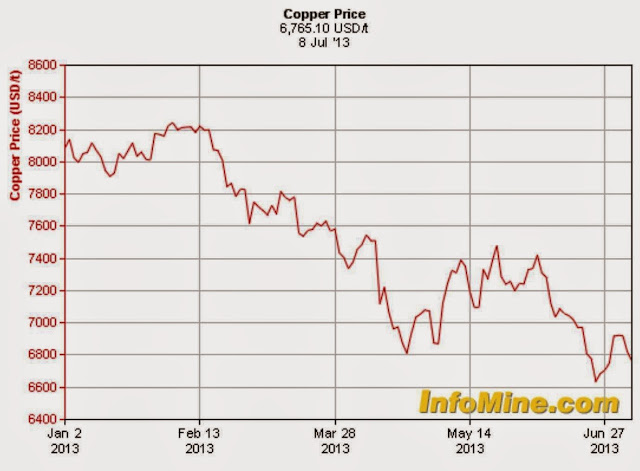

Copper prices continue falling. It has now fallen by 15% this year. This continues a trend which has seen the red metal losing $3000 per tonne over the last two years. That fall has coincided with a slowdown in China's growth. The Chamber of Mines recently said if low copper prices continue "the industry will have to review its operations in the country". In particular, "mining firms might be forced to address their operations through cutting down expenses which include labour costs".

We have reason to be concerned because the fall in prices will continue as China's economy slows down. China's growth rate is still well above 7 per cent a year, but a slowdown is happening, and the near 10 per cent growth of the previous decade is gone.

It is inevitable that some mining closures may occur if the trend continued (as was the case in 2009 ). But there's reason to be hopeful. For one thing the signals from China is that they are seeking to hold back grouwth around that level. Hence the copper prices are unlikely to ever fall to 2008/9 levels because the drivers this time round are different. This is China re-adjusting within the general growing trajectory rather than a meltdown in the global economy.

More importantly our experience in 2008/9 shows that though output declined Zambia was still able to maintain growth around 6%, against expectations, largely due to strong performance in construction and agriculture.The policy response at that time was quite decisive with the Banda government moving swiftly to secure mining closures and make effective use of counter-cyclical policy with costly concessions to mining companies.

The PF government needs to be prepared for these uncertain times and begin planning for contingencies in case things get worse. They have the advantage of that any reduction in revenue levels from low copper prices, against the counter-factual, should be offset by ramp up in mining production in general - assuming the prices remain broadly reasonable.

The key is ensuring fiscal prudence now so that we have sufficient headroom for counter cyclical policy should the need arise. Hence it is worrying that Government has been committing itself to huge wage rises, supported rampant bye-elections; and, is borrowing like there's no tomorrow. Now is not the time for such excesses.

Equally important is that GRZ should be wary of tinkering too much at this stage with the mining fiscal regime. In times of uncertainty, stability is the watch word. It needs to resist the pressure from all corners for arbitrary changes, including mining companies.

And of course we should note that in the long term structural demand for copper is positive. There are good reasons to believe that strong demand from China and other emerging economies in particular may continue for several decades, although the adoption of new technologies could see a lower degree of resource intensive output in these countries over time.

Furthermore, productivity advances are still helping to contain the world price of manufactured goods, and a reduction in the price of some services is also probable as the tradability of services in an increasingly globalised economy becomes more widespread. While these various trends continue, they could support the continuation of relatively high real prices for metals and other resources for some time yet.

ABOUT THE AUTHOR

Chola Mukanga | Economist | Writer

Copyright © Zambian Economist 2013